India didn’t wait to get rich

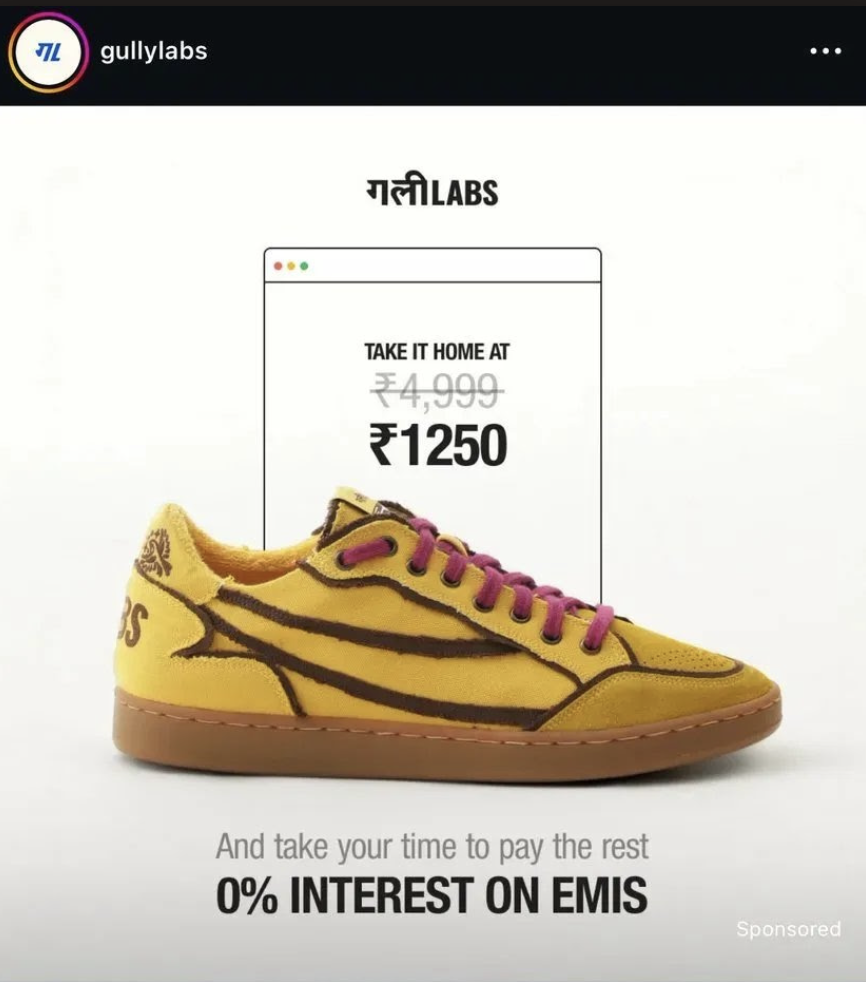

GullyLabs, an Indian sneaker brand, popped up on my instagram feed with an ad for their new pair of shoes. What struck me was neither the design nor the price, but the line in bold underneath: Take it home at ₹1,250. Take your time to pay the rest. 0% interest on EMIs.

I kept staring at it to try and make sense of the jumbled thoughts in my brain - “Is that how my generation is consuming? Buying sneakers on an EMI!?”

…which led me to a rabbit hole, and hence, this long article.

In all of the consumption reports on India, there’s a version of India’s economic story that gets told a lot. The one where a billion-plus people are slowly waking up to consumption, climbing a ladder from frugality to aspiration. Disposable incomes are rising, the middle class has expanded, and India is aspirational now, according to all of these reports.

All of that is true, but it’s also incomplete.

India has never had a consumption problem. The desire was always there, for the same products the wealthy were buying. What rather existed was a timing and liquidity problem, which limited consumption.

Every economy tries to close the gap between what people want and what they can afford. The conventional way is to grow incomes, raise living standards, and wait for means to catch up to desire. India did that too. But parallel to that story, there’s another one that doesn’t get enough credit.

India’s brands and companies figured out that you don’t have to close the gap between desire and means to drive consumption. You just have to make that gap feel invisible at the moment of consumption.

And it’s happened across the years in three distinct ways, each one hiding the gap more completely than the last. Please allow me to explain.

Part 1: Shrink the price and the unit

Walk into any kirana store in a small Indian town in the 1990s and look at the wall behind the counter. Row after row of small foil packets, pinned or hanging from a wire rack. Clinic Plus. Pantene. Dove. Sunsilk. Nescafé. The same brands you’d find in the bathroom cabinet of a middle-class home in South Delhi back in the day (and some even today), just in a different form. Small flat sachets, each containing enough for a single use, priced at ₹1 or ₹2.

What this meant is that a domestic worker earning ₹3,000 a month could buy the same Pantene as her employer. Not a cheaper version, but the same product! She just bought one wash at a time instead of one bottle at a time. A student in a hostel could have the same Nescafé as the professionals in the office next door, one cup, one sachet, torn open at the corner and stirred into hot milk in a steel tumbler

Everyone called it democratisation. I think it’s the wrong word because it implies the said gap is closed when it clearly isn’t, because the domestic worker didn’t get richer. What happened was that the product restructured itself around how money actually existed in her life. A ₹100 bottle required ₹100 at one moment. The sachet matched the unit of purchase to the unit of income. Same Pantene, just less of it, right now, at a price that works today.

If I have to draw a parallel to 2026, I’d look at the soda industry.

My dad still refers to Coke as “Campa.” So did my grandfather. Before Coke and Pepsi arrived, there was a small ₹10 PET bottle, same black colour, same fizz, at a mere ₹10 (which seems to be the magic number in India). Reliance relaunched Campa in 2023 at ₹10, and now it’s sponsoring a team in IPL with its comeback. Coca-Cola and Pepsi had to cut their prices to compete with Campa within a year of its relaunch.

We’ve also seen Lahori Zeera build a ₹500 crore+ business on the same price point by prioritising kirana shelves over e-commerce/quick commerce. Sting also came in at ₹20 when its market competitor, Redbull, was priced at ₹125. It offered the same caffeine rush in a plastic bottle instead of a tin can, and took away 90% market share from RedBull in six years.

All of these examples rely on the same instinct of “sachetising” a premium product into something that’s quick, affordable, and easy to consume - despite the difference in categories.

Part 2: Shrink the unit and the time commitment

The first evolution was physical goods. The second is digital, and here something new enters. It’s not just the unit and price that shrink. The time commitment shrinks too, and technology is what makes this possible.

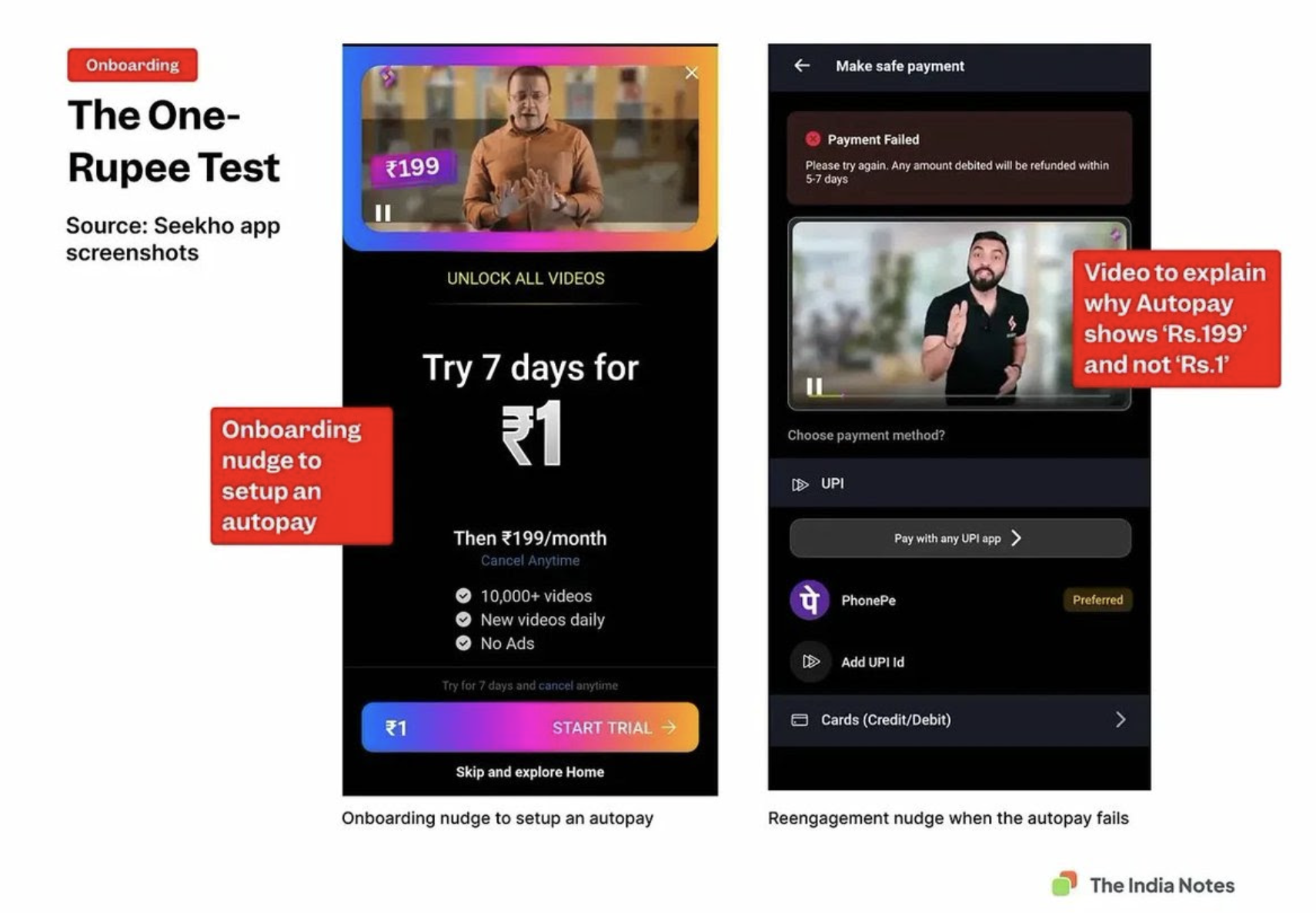

If you didn’t grow up in a Tier 1 city and you wanted to learn English, you needed a tutor. Hours of your week, thousands (and lakhs in some cases) of rupees, a significant commitment. Today, you can do it on @thespeakx for ₹299 a month, with a few minutes of AI conversation practice daily. Seekho does the same for everything else: share market basics, digital skills, government job prep, at ₹199 a month, which roughly ~₹6 a day. Seekho even ran a campaign offering a seven-day trial for ₹1, the same logic as the shampoo sachet applied to learning.

Entertainment is the same story. A Bollywood film meant ₹300-500 for the ticket, petrol, an entire evening commitment by a family, and expensive popcorn, which has always been treated as a luxury.

Kuku TV is ₹1.2 a day. Episodes of 90 seconds to 2 minutes, built for the commute, the lunch break, and the ten minutes before sleep. Platforms like ReelSaga are also growing fast in this space. India became the world’s number one market for short drama app downloads in July 2025, with 21 million installs in a single month. Original Hindi films dropped 37% in 2024. I don’t claim that there’s a direct causation of micro drama apps that led to the decline of Bollywood (like there is with OTT) over the last two years, but there’s definitely a strong correlation between the two.

In my opinion, the 90-second episode is to Bollywood what the ₹1 sachet was to the ₹100 shampoo bottle. Not replacing, but restructuring the unit so the same desire for story and entertainment can be met in the moments of time and money that actually exist. And it’s worth noting: this isn’t the same as YouTube or Instagram, where all content is free for everyone. These apps give you a story you paid for. The exclusivity is part of what’s being purchased. It’s the same reason a cinema ticket always felt different from watching TV at home.

If I can make a stretch, I’d think quick commerce belongs in this same bucket, because technology is exactly what makes it work. Big Bazaar & D-Mart trained a generation to shop in bulk as the monthly ritual for every middle-class family. Qcomm collapsed that entirely where the average order is ₹600, frequency per user is 3-5 times a week, and “micro” purchasing is possible. You’d never go to Big Bazaar to just buy a tray of eggs and a bread pack, but that’s exactly what you’d do on qcomm. The ticket size, the friction, the time, all of it has been fundamentally restructured by technology.

The common thread across all three - education, entertainment, groceries - is that tech didn’t just make these things cheaper necessarily, but it definitely compressed the time you need to commit to consuming them. And when you compress both the price and the time, you open up consumption to an enormous number of people.

Part 3: Shrink the price, but keep the unit

Everything in the first two parts involved a trade-off. You got less shampoo, shorter episodes, and a smaller basket. The unit shrank, so you were made aware that you were consuming less.

Then India figured out how to remove even that trade-off.

If you remember the ad from Gully Labs I had brought up at the start of the article, that is exactly the case point for this argument.

When you apply for this EMI, you don’t get a smaller shoe from Gully Labs. You don’t get one shoe today and one next month. You get the whole pair, right now, when you walk out. The only thing restructured is the payment.

Bajaj Finserv also lets you buy Nike shoes under ₹10,000 across monthly instalments. A startup was giving travel loans if you were attending a Coldplay concert in a different city.

All of this to me, to say the least, is bonkers. We grew up thinking EMI was high-ticket items - for the cars you buy, the home loans, the expensive appliances. My generation is doing it for..sneakers.

The personal loan balance outstanding in India was ₹30.1 lakh crore in FY21. By FY25, it had reached ₹59.5 lakh crore. Nearly doubled in four years. On the other side of that ledger, India’s net household savings peaked at 11.7% of GDP in FY21, the pandemic year when there was nowhere to spend, and fell to 5.2% of GDP by FY24.

The interesting bit here is the psychological point. When I bought a ₹1 sachet, everyone could see I was buying a sachet. When I bought a ₹10 Campa in a plastic bottle instead of a ₹40 Coke in a fancy tin can, everyone could see the smaller bottle. The constraint and my purchasing power were visible. But with something like sneakers, there is no additional signal. I am wearing the same shoes as someone who paid ₹4,999 outright. They cannot see my constraint. Hell, I cannot even feel my constraints at the moment of wearing them. The performance of the identity and the identity itself have become, at every visible moment, indistinguishable.

All of this is thirty years of continuous financial engineering, which is often perceived as product innovation, consumer insight, and technological progress. And in many ways, it is all of those things too. Seekho genuinely democratised access to learning. Quick commerce genuinely made everyday life more convenient. The sachet genuinely put branded products in the hands of people who wanted them. None of this is cynical.

But it is worth sitting with what we’ve actually built. A country where the infrastructure for feeling affluent has grown faster than the infrastructure for being affluent. Where a generation has grown up with tools so good at hiding the gap between desire and means that the gap has become almost imperceptible at the only moment most people are paying attention, which is the moment they decide to buy. Hence, the gap between desire and means hasn’t closed. The infrastructure for making feel invisible at the time of consumption has just gotten very, very good.

The desire was never India’s problem. It never needed to be manufactured. It was always there, pressing against whatever constraint existed, looking for the unit of purchase or the payment structure that would finally let it through. What changed, across thirty years, is that we got extraordinarily good at building that unit - at finding the format, the price, the instalment plan that would let desire act on itself today, and deal with the arithmetic tomorrow.

India didn’t wait to get rich. It just kept building better ways to feel like it already was.